Overview

- AI-powered fraud is on the rise in the US, and many financial platforms are at risk of billions in fraud losses

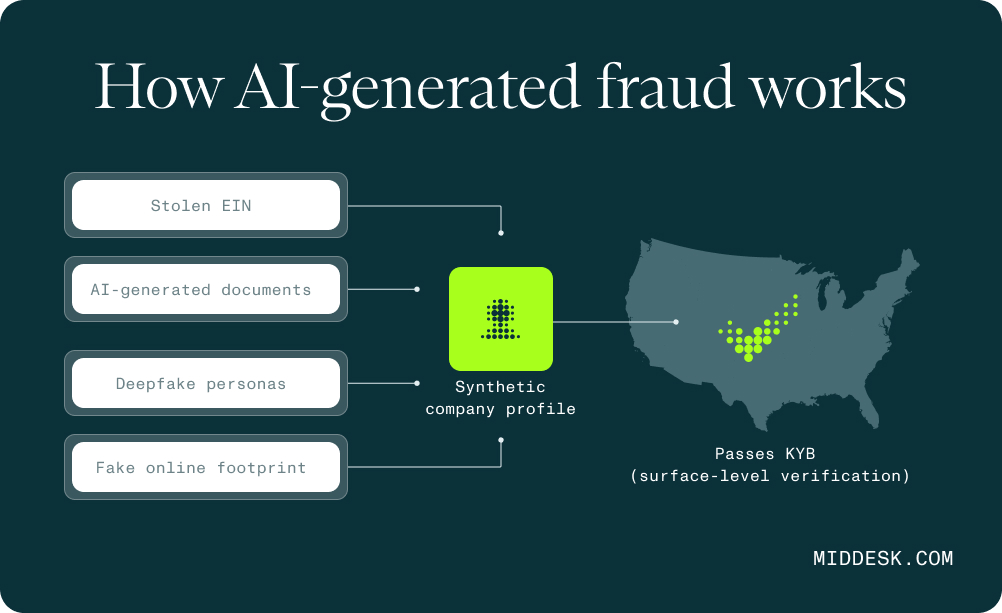

- Fraudsters use synthetic identities, AI-generated documents, deepfakes, Fraud-as-a-Service tools, and fake online footprints

- Modernizing your KYB/KYC process to account for AI fraud is the only way to keep fraud off your platform

Fraud is evolving at a breakneck pace. While forging business documents and assuming fake identities once required significant effort and skill, generative AI has drastically lowered the barrier to entry for business fraud. Today, criminals can use AI tools to spin up synthetic identities, create authentic-looking documents, and even build entire fictitious companies with convincing online footprints.

The result has been a wave of AI-generated fraud that traditional Know Your Business (KYB) and Know Your Customer (KYC) checks struggle to detect, making it difficult for compliance teams to distinguish real businesses and owners from fraudulent ones.

How AI-enabled fraud works

AI-powered fraud occurs when fraudsters use modern AI tools to create synthetic identities that can pass surface-level KYB and KYC checks when trying to onboard on a financial platform, like opening a bank account, or securing a loan from a lender.

Fraudsters use AI video and photo software to generate fake documents, establish fake identities, and deepfake their way onto platforms. KYC AI fraud occurs when fraudsters do this as individuals, and KYB AI fraud is when they create synthetic companies, which usually provides them access to more money.

What is a KYB/KYC bypass?

A KYC bypass is when a fraudster uses tools to create a synthetic identity as an individual that is specifically formed to pass a KYC check in a financial platform. This requires knowledge about what types of KYC checks are being done during onboarding, and then building a synthetic identity that can pass those checks.

A KYB bypass is the same thing, but when the fraudster creates a synthetic business identity that can pass a KYB check. They impersonate business owners, or the business itself, to onboard as a commercial customer, unlocking access to greater limits on financial transactions, or bigger loans from lenders.

How fraudsters find loopholes in KYB/KYC checks

Fraudsters will often look at platforms individually to perform a more effective KYB/KYC bypass. They will look into what types of documentation the platform asks for (and what they don’t), and look for holes in the verification process. They then use AI to mimic the exact parameters of what the platform is looking for, and provide that during onboarding.

Expert tip: The best way to combat this is to verify submitted information against authoritative and alternative databases to ensure that submitted information is real, and not AI-generated.

The AI-enabled fraud landscape: new tools, new threats

Recent reports confirm what many in compliance have already seen first-hand: AI-powered fraud is surging. One report found that deepfake incidents across industries jumped tenfold from 2022 to 2023.

Warning: The situation has deteriorated to the point that, by late 2024, the U.S. Financial Crimes Enforcement Network (FinCEN) alerted the financial services industry to a significant rise in the use of deepfake media that “often involve criminals altering or creating fraudulent identity documents to circumvent identity verification and authentication methods.”

Here are some of the key methods fraudsters are using to bypass KYB / KYC verification:

Synthetic identities

AI makes synthetic identity fraud easier than ever to blend real and fake information into a “Frankenstein” identity. For individual KYC, this might be combining a stolen Social Security number with a fictitious name and AI-generated photo. In the KYB context, fraudsters can generate synthetic business identities by mixing valid data (e.g., a real Tax ID number) with fake details like bogus executives or addresses. These synthetic profiles often slip past basic due diligence, enabling bad actors to open bank accounts or obtain credit under a fake business that looks legitimate on paper.

AI-generated documents

Modern generative models (including image generators and advanced editing tools) can produce fake documents that are virtually indistinguishable from the real thing. This includes forged incorporation papers, business licenses, bank statements, and tax forms, all bearing realistic seals, fonts, and signatures.

For example, a fraudster can use AI to create a fake certificate of incorporation with an official-looking government seal and accurate registrar details. These AI-enabled document forgeries are already being used to bypass KYC and KYB checks at banks and fintechs.

In one survey, 94% of insurance claims handlers suspected at least 5% of the claims they see have been manipulated with AI tools — and there’s no reason to think that AI-assisted document fraud will slow down anytime soon.

Deepfake personas

Verifying the identity of a business representative via video call or recorded verification is no longer foolproof. AI-driven deepfake technology can create hyper-realistic video and audio of a person that doesn’t exist — or impersonate a real executive. Imagine a fraudster using an AI “face swap” to appear as someone else on a webcam, or cloning a CEO’s voice to pass a phone verification.

In one startling case from early 2024, a Hong Kong company’s employee was tricked into transferring $25 million after fraudsters hosted a video meeting in which they deepfaked the likeness of the company’s CFO and other colleagues. This heist shows how far deepfake realism has come, and the same techniques can be used to fool companies — particularly financial services companies and marketplaces — during the customer onboarding process.

Selling Fraud-as-a-Service (FaaS) KYB/KYC bypass software

Fraudsters are building and selling their own KYB/KYC bypass tools that can use AI to commit fraud on banking, lending, and other financial platforms. These services are sold online and will include a package of fake documents and credentials that fraudsters can use to try to onboard on a platform.

Fake online footprints

A convincing business fraud often requires more than just documents. The scheme also needs an identity that checks out under light scrutiny. To that end, AI is also being used to spin up fake websites, social media profiles, and even customer reviews for shell companies. With AI tools, a fraudster can quickly build a professional-looking business website populated with entirely fabricated content, or generate LinkedIn profile photos for a roster of fake employees (complete with AI-written bios).

These tactics add credibility during manual KYB reviews. A quick internet search might surface a legitimate-seeming company page or press release, duping analysts into thinking that if it has an online presence, it must be real. Voice cloning tools also let scammers handle verification phone calls in the guise of someone else, providing further credence for the fake business’s story.

Clearly, AI has armed fraudsters with both technological sophistication and the power to scale up their efforts in very little time. Unfortunately, the business verification technology at many organizations is not up to the task, as they still rely on PDFs and manual due diligence alone. Generative AI is allowing bad actors to exploit these shortcomings. Their fake businesses look more legitimate than ever, at least on first pass.

How to combat synthetic identity fraud in business onboarding

Discover how financial institutions, fintechs, and marketplaces are deploying multi-layered defense strategies that catch what conventional systems miss.

Discover how financial institutions, fintechs, and marketplaces are deploying multi-layered defense strategies that catch what conventional systems miss.

Modernizing KYB: how to fight back against AI fraud

Industry analysts predict that by 2027, AI-enabled fraud losses could reach $40 billion in the US alone (up from $12.3B in 2023). The good news is that as fraudsters adopt AI, so can you and your organization. Compliance and operations teams are not helpless — new strategies and technologies can bolster KYB defenses in this new era.

These best practices can propel your KYB program into the future:

1. Automate checks, and verify at the source

Fraudsters are getting better at mimicking legitimacy, which makes relying on documents alone risky. Instead, build your KYB process around direct-from-source data. That means pulling business registration details directly from government registries, checking license status with issuing authorities, and confirming ownership structures through trusted databases.

Automated workflows can flag mismatches and incomplete records in real time, reducing manual work while increasing accuracy.

2. Don’t stop at the business — verify the people behind it

Modern KYB programs also account for the individuals who own or control a business. That includes identity validation, sanctions screening, and confirming that listed beneficial owners are real, traceable individuals — not synthetic identities. If someone claims 25% ownership, you should be able to corroborate their existence through reliable data sources like credit headers or public records.

3. Look for hidden connections and patterns

Fraud often takes place within networks of attackers. If multiple businesses use the same phone number, IP address, or incorporation agent, those are signals worth investigating. Graph analysis or link detection tools can help uncover when applicants are part of a coordinated ring — something that’s easy to miss when each application is reviewed in isolation.

Looking at the bigger picture helps surface fraud rings and prevent repeat attempts across different accounts or platforms.

4. Monitor continuously, not just at onboarding

One-and-done verification isn’t enough. A business that looks legitimate at onboarding can change ownership, fall out of good standing, or become compromised months later. That’s why ongoing monitoring for things like status changes, new adverse media, or irregular activity is key to staying ahead of evolving risk. Continuous KYB helps detect “sleeper” fraud and keeps your customer profiles up to date over time.

5. Train your team to spot AI-assisted red flags

Technology matters, but human judgment still plays a key role. Your teams should know how to recognize signs of AI-generated documents, synthetic identities, and deepfakes. That might mean training frontline reps on verification techniques (e.g., how to test liveness during video calls) or sharing examples of suspicious applications that slipped through the cracks. The more eyes looking for subtle red flags, the harder it becomes for fraud to get through.

6. Use purpose-built tools to keep up with emerging risks

Today’s fraud prevention requires more than static checklists. Leading KYB platforms are evolving to meet the moment — combining direct data access, machine learning, and continuous monitoring to help compliance teams make faster, more confident decisions. Look for tools that integrate identity and business verification, surface risk signals automatically, and update with new fraud patterns as they emerge.

Modernize your KYB process in the era of AI fraud

Companies, especially in fintech and financial services, cannot rely on yesterday’s KYB playbook to counter today’s threats. By investing in modern KYB platforms, integrating continuous monitoring, and adopting a layered, identity-centric approach, organizations can start to close the gaps that AI-driven fraudsters are exploiting.

The companies that move fastest to modernize their KYB and fraud prevention processes will be best positioned to thrive in this new landscape. As fraud continues to evolve, a forward-thinking compliance strategy that blends human judgment with smarter technology will be your strongest asset to stay one step ahead.

Middesk checks business identity information at the source — in the SOS database — with the freshest possible data to verify the information provided by your customers during onboarding is accurate. Set up a demo and see how we do it:

Combat AI-powered fraud by validating business identities at the source

Don’t rely on customer-provided documents.

Don’t rely on customer-provided documents.